参考链接:https://www.backtrader.com/blog/posts/2015-09-25-tickdata-resample/resample-tickdata/

backtrader could already do resampling up from minute data. Accepting tick data was not a problem, by simply setting the 4 usual fields (open, high, low, close) to the tick value.

backtrader已经可以从微小数据进行重新采样。接受点数据不是问题,只要简单地将4个常用字段(open, high, low, close)设置为点值。

But passing the tick data to be resampled produced the same data again. As or release 1.1.11.88 this is no longer so. Now

但是传递要重新采样的tick数据会再次产生相同的数据。现在已经不是1.1.11.88版本了。

-

TimeFrame (backtrader.TimeFrame) has been extended to contain constants and names for “Ticks”, “MicroSeconds” and “Seconds”

- 时间帧(backtrader.TimeFrame)被扩展为包含“Ticks”、“MicroSeconds”和“Seconds”的常量和名称。

-

Resampling can manage the 3 aforementioned timeframes and sample them up.

- 重新采样可以管理上述3个时间框架和样本。

Note

Because tick data is the lowest possible timeframe it can actually be “compressed” (n bars to 1 bar) but not be sampled up from a smallest timeframe.

因为tick数据是最低可能的时间框架,它实际上可以被“压缩”(n条到1条),但不能从最小的时间框架进行采样。

The new release contains a small tickdata.csv sample added to the sources data a new sample script resample-tickdata.py to play with it.

新版本包含一个添加到源数据的小示例tickdata.csv,一个新的示例脚本resams -tickdata.py来处理它。

Note

Updated the script to use the new Cerebro.resampledata method which avoids the need to manually instantiate a backtrader.DataResampler

更新了脚本以使用新的Cerebro.resampledata方法,避免了手动实例化backtrader.DataResampler

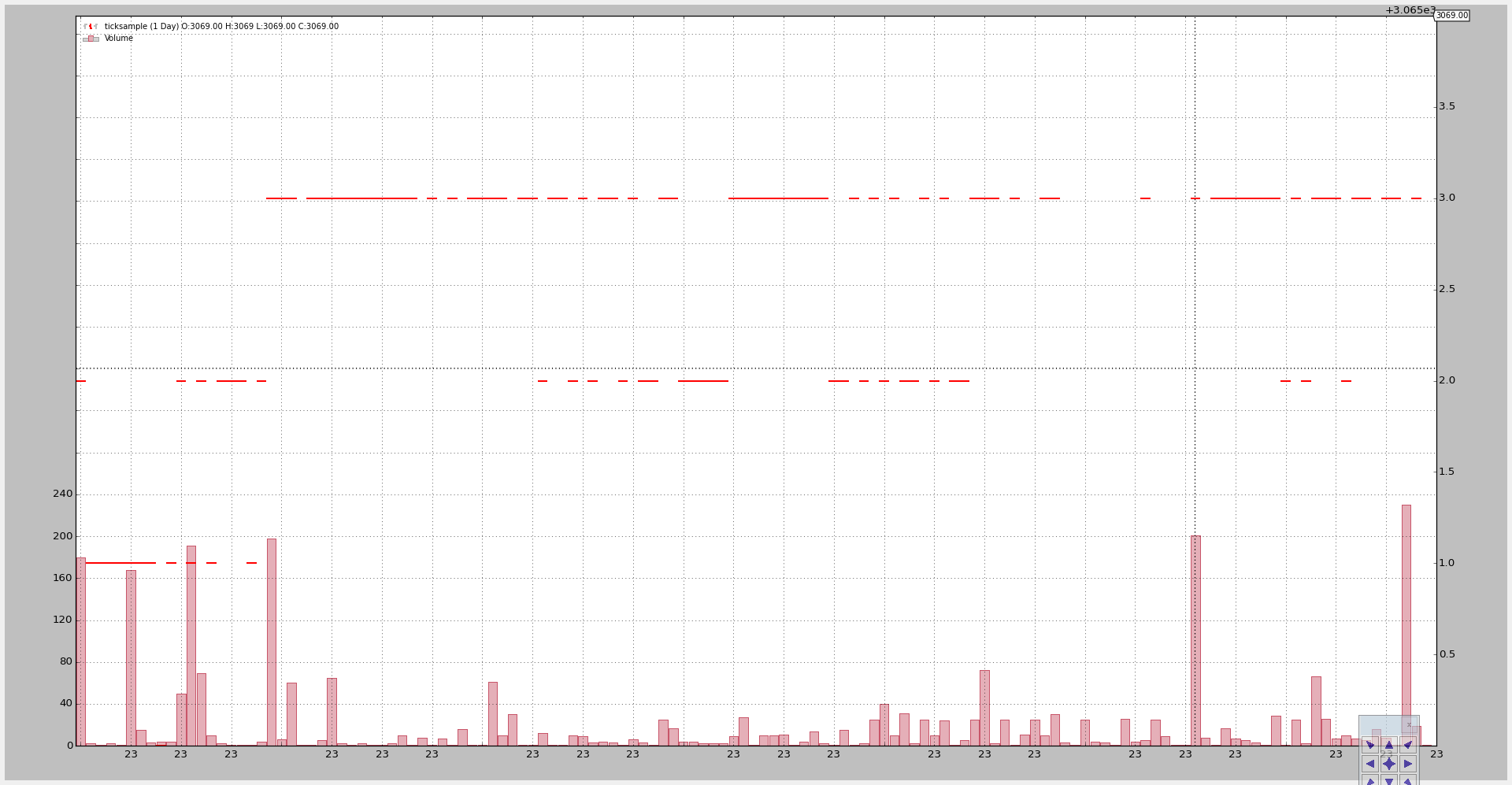

The default execution doesn’t touch the data:

默认的操作不会接触到数据

$ ./resample-tickdata.py

Producing this chart:

产生的图形:

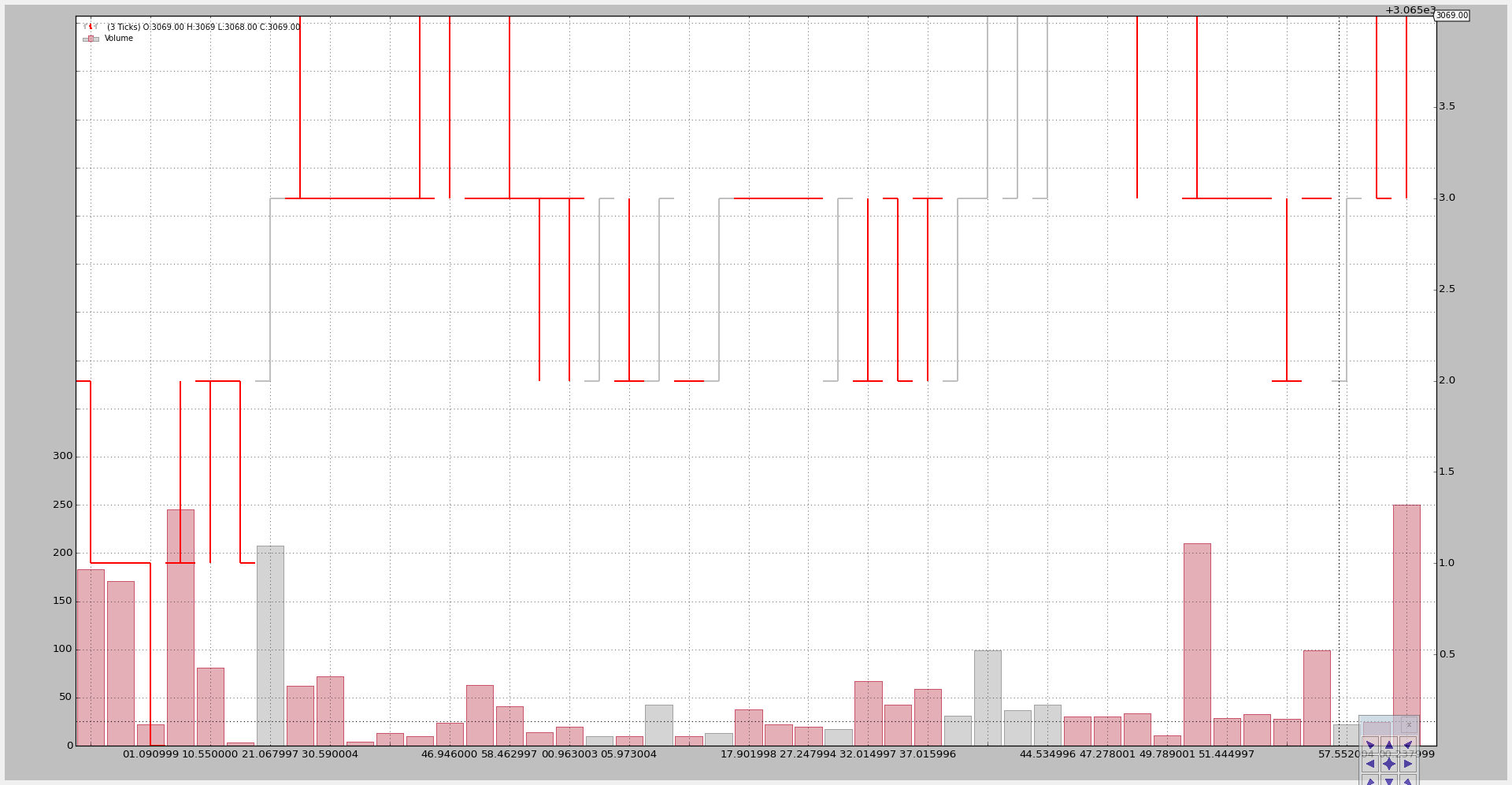

Compressing 3 ticks to 1:

压缩三个ticks到1个:

$ ./resample-tickdata.py --timeframe ticks --compression 3

Producing this chart:

After the compression we no longer have single “ticks” but “bars”.

在压缩之后,我们不再有单一的“刻度”,而是“条”。

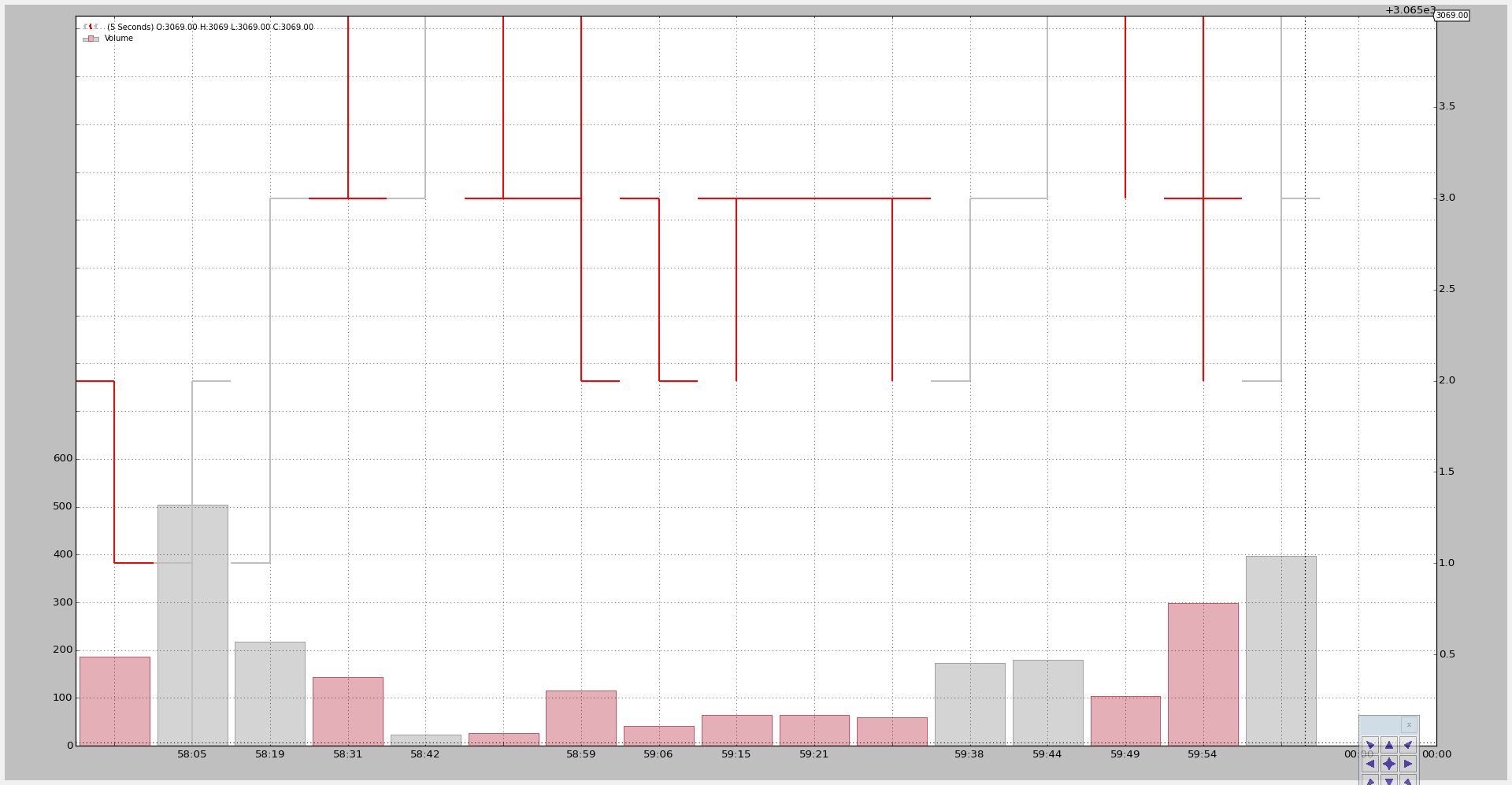

Now compressing to seconds and 5 bars compression:

现在压缩到秒和5条压缩:

$ ./resample-tickdata.py --timeframe seconds --compression 5

With a new chart:

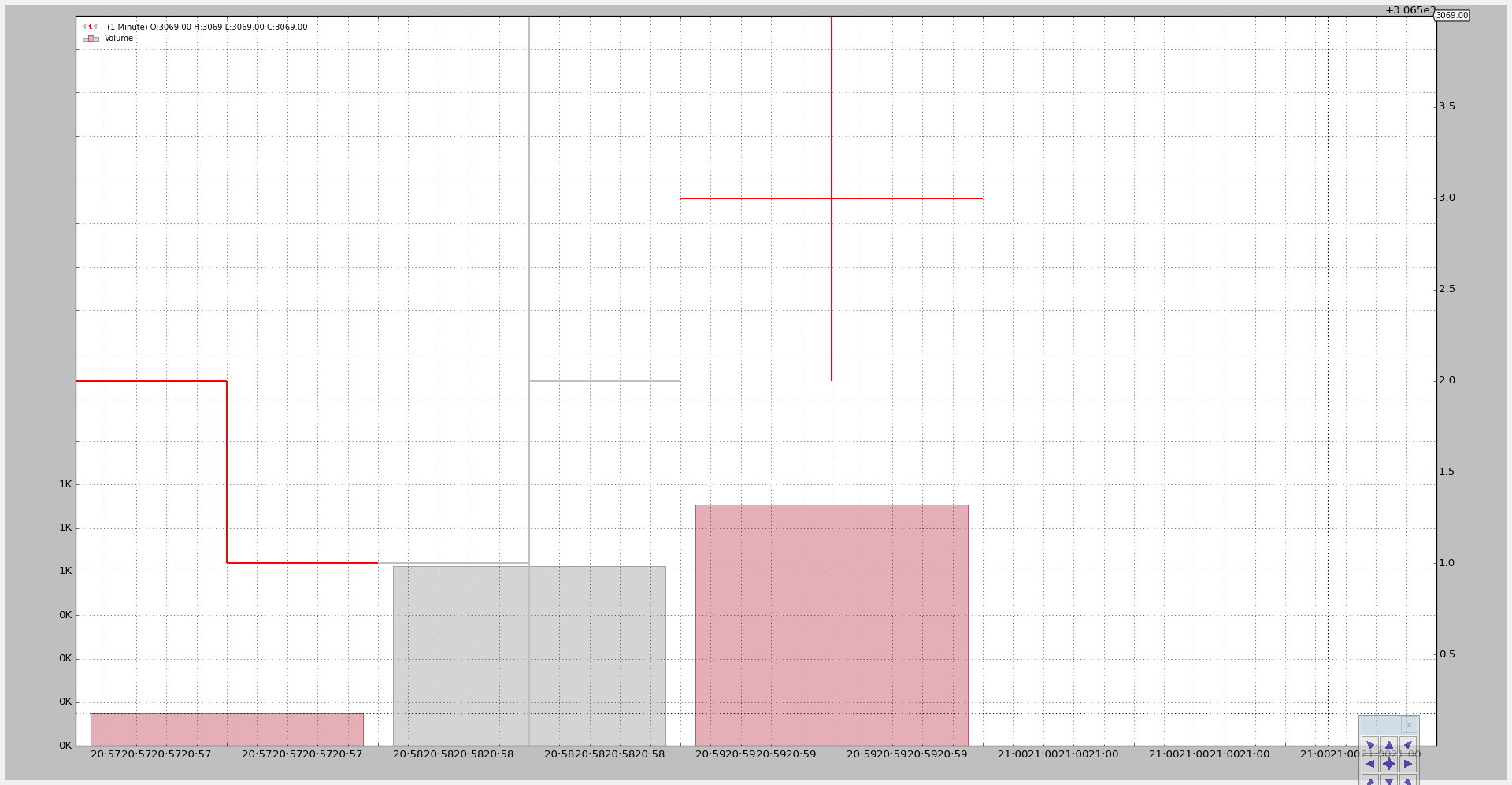

And finally to minutes. The sample data contains tick data from 4 different minutes (the last tick in the file is the only tick for the 4th minute):

最后是分钟数据。示例数据包含4分钟的tick数据(文件中的最后一个tick是第4分钟的唯一tick):

$ ./resample-tickdata.py --timeframe minutes

With a 4 bars (at the top it can be seen the final price was 3069). The 4th bar is a single point given for this minute a single tick is present in the file.

4个bars(在顶部可以看到最终价格是3069)。第4个bar是为这分钟给定的一个单点,文件中有一个单点。

The script usage:

$ ./resample-tickdata.py --help

usage: resample-tickdata.py [-h] [--dataname DATANAME]

[--timeframe {ticks,microseconds,seconds,minutes,daily,weekly,monthly}]

[--compression COMPRESSION]

Resampling script down to tick data

optional arguments:

-h, --help show this help message and exit

--dataname DATANAME File Data to Load

--timeframe {ticks,microseconds,seconds,minutes,daily,weekly,monthly}

Timeframe to resample to

--compression COMPRESSION

Compress n bars into 1

And the code.

from __future__ import (absolute_import, division, print_function,

unicode_literals)

import argparse

import backtrader as bt

import backtrader.feeds as btfeeds

def runstrat():

args = parse_args()

# Create a cerebro entity

cerebro = bt.Cerebro(stdstats=False)

# Add a strategy

cerebro.addstrategy(bt.Strategy)

# Load the Data

datapath = args.dataname or '../../datas/ticksample.csv'

data = btfeeds.GenericCSVData(

dataname=datapath,

dtformat='%Y-%m-%dT%H:%M:%S.%f',

timeframe=bt.TimeFrame.Ticks,

)

# Handy dictionary for the argument timeframe conversion

tframes = dict(

ticks=bt.TimeFrame.Ticks,

microseconds=bt.TimeFrame.MicroSeconds,

seconds=bt.TimeFrame.Seconds,

minutes=bt.TimeFrame.Minutes,

daily=bt.TimeFrame.Days,

weekly=bt.TimeFrame.Weeks,

monthly=bt.TimeFrame.Months)

# Resample the data

data = cerebro.resampledata(data,

timeframe=tframes[args.timeframe],

compression=args.compression)

# add a writer

cerebro.addwriter(bt.WriterFile, csv=True)

# Run over everything

cerebro.run()

# Plot the result

cerebro.plot(style='bar')

def parse_args():

parser = argparse.ArgumentParser(

description='Resampling script down to tick data')

parser.add_argument('--dataname', default='', required=False,

help='File Data to Load')

parser.add_argument('--timeframe', default='ticks', required=False,

choices=['ticks', 'microseconds', 'seconds',

'minutes', 'daily', 'weekly', 'monthly'],

help='Timeframe to resample to')

parser.add_argument('--compression', default=1, required=False, type=int,

help=('Compress n bars into 1'))

return parser.parse_args()

if __name__ == '__main__':

runstrat()

经过调试,可以在策略里面调试使用。后面就可以通过这种格式进行时间的压缩。