作业说明

Exercise 1,Week 2,使用Octave实现线性回归模型。数据集 ex1data1.txt ,ex1data2.txt

单变量线性回归必须实现,实现代价函数计算Computing Cost 和 梯度下降Gradient Descent。

多变量线性回归可选,实现 特征Feature Normalization、代价函数计算Computing Cost 、 梯度下降Gradient Descent 和 Normal Equations 。

文件清单

- ex1.m

- ex1_multi.m

- ex1data1.txt - ex1.m 用到的数据组

- ex1data2.txt - ex1_multi.m 用到的数据组

- submit.m - 提交代码

- [*] warmUpExercise.m

- [*] plotData.m

- [*] computeCost.m

- [*] gradientDescent.m

- [+] computeCostMulti.m

- [+] gradientDescentMulti.m

- [+] featureNormalize.m

- [+] normalEqn.m

* 为必须要完成的

+ 为可

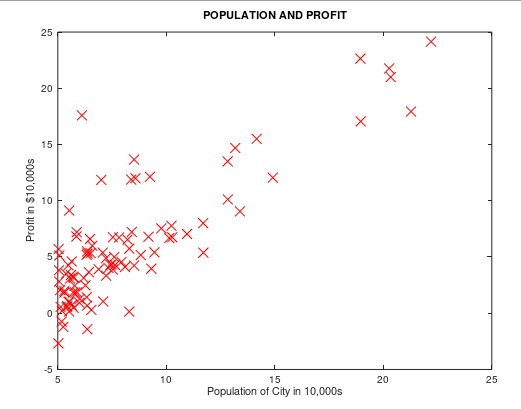

背景:假设我们现在是个连锁餐厅的老板,已经在很多城市开了连锁店(提供训练组),现在想再开新店,需要通过以前的数据预测新开的店的收益。

ex1data1.txt 提供所需要的训练组,第一列是城市人口,第二列是对应的收益。负值代表着亏损。

结论

当数据的特征维度比较小的时候,使用正规方程方法不需要进行特征归一化,而且结果稳定。梯度下降有可能得到局部最优解,导致结果不同。

注意矩阵计算的一些问题,求和前面一项需要转置。

必做题 单变量线性回归

一、warmUp

单变量线性回归入口在ex1.m

warmUpExercise.m

A = eye(5)

二、绘制数据图

我实现的 plotData.m:

20 plot(x,y,'rx', 'MarkerSize', 10); 21 xlabel('Population of City in 10,000s'); 22 ylabel('Profit in $10,000s'); 23 title('POPULATION AND PROFIT');

ex1.m 中的调用:

1 %% ======================= Part 2: Plotting ======================= 3 data = load('ex1data1.txt'); 4 X = data(:, 1); y = data(:, 2); 5 m = length(y); % number of training examples 6 8 plotData(X, y);

运行效果如下:

三、代价函数

我实现的 computeCost.m:

1 function J = computeCost(X, y, theta) 7 m = length(y); % number of training examples 8 10 J = 0; 11 17 predictions = X * theta; % predictions of hapothesis on all m examples 20 sqrErrors = (predictions - y) .^ 2; % squared errors .^ 指的是对数据中每个元素平方 21 22 J = 1 / (2 * m) * sum(sqrErrors); 27 end

四、梯度下降

我实现的 gradientDescent.m

矩阵性质:(AB)T =BTAT

1 function [theta, J_history, theta_history] = gradientDescent(X, y, theta, alpha, num_iters) 7 m = length(y); % number of training examples 8 J_history = zeros(num_iters, 1); 9 theta_history = zeros(2, num_iters); % 【改动】使用 2×iteration维矩阵,保存theta每次迭代的历史 10 11 for iter = 1:num_iters 12 20 % 这里为了方便理解 拆的比较细,可以组合成一步操作 theta = theta - (alpha / m) * X' * (X * theta - y) 21 % prediction h(x) m×2矩阵 * 2×1向量 = m维列向量 22 predictions = X * theta; 23 % error h(x)-y m维列向量 24 errors = predictions - y; % 25 % derivative of J() m维行向量 * m×2矩阵 = 2维列向量 26 lineLope = X' * errors; 27 % theta 2维列向量 28 theta = theta - (alpha / m) * lineLope; % 37 38 J_history(iter) = computeCost(X, y, theta); % Save the cost J in every iteration 39 theta_history(:,iter) = theta; % 给theta_history 第iter列赋值 40 end 41 42 end

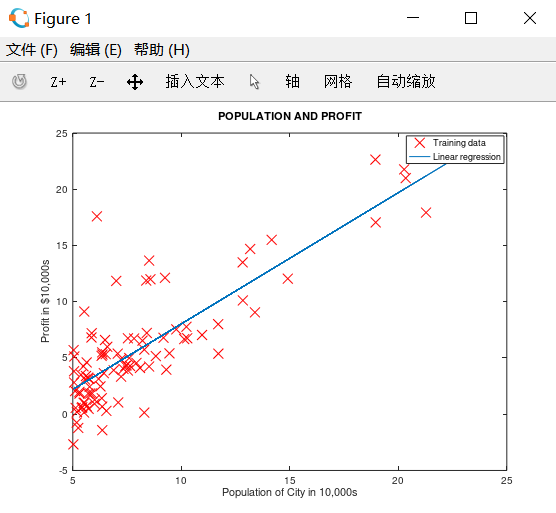

五、绘制预测曲线

ex1.m 中的调用:

1 %% =================== Part 3: Cost and Gradient descent =================== 2 3 % 设置 X 和 theta 4 X = [ones(m, 1), data(:,1)]; % Add a column of ones to x 5 theta = zeros(2, 1); % initialize fitting parameters 6 7 % 设置迭代次数和学习速率 8 iterations = 2000; 9 alpha = 0.01; 10 12 % compute and display initial cost 计算theta=[0;0]时代价 13 J = computeCost(X, y, theta);16 17 % further testing of the cost function 计算theta=[-1;2]时代价 18 J = computeCost(X, y, [-1 ; 2]);21 25 fprintf(' Running Gradient Descent ... ')27 % 【改动1】改为获取多个返回值,J_history保存每次迭代的代价,theta保存每次迭代的theta0和theta1 28 % 原:theta = gradientDescent(X, y, theta, alpha, iterations); 29 [theta,J_history,theta_history] = gradientDescent(X, y, theta, alpha, iterations); 30 36 37 % Plot the linear fit 在数据图上绘制最终的拟合直线 38 hold on; % keep previous plot visible 39 plot(X(:,2), X*theta, '-') 40 legend('Training data', 'Linear regression') 41 hold off % don't overlay any more plots on this figure

运行结果如下:

四、绘制cost和theta变化曲线

自己加的功能。在ex1.m中增加以下代码,绘制图像。展示迭代过程中 cost 和 theta 的变化曲线

1 % --------------【改动2】绘制代价和theta变化曲线 start -------------- 2 fprintf('Size of J_history saved by gradient descent: '); 3 fprintf('%f ', size(J_history)); 4 iterX = [1:iterations]'; % 生成图像横坐标,迭代次数 5 6 % 绘左侧图,展示迭代过程中代价的变化曲线 7 subplot(1,2,1); 8 plot(iterX, J_history, '-','linewidth',3); % 绘制代价函数曲线 9 title('cost of each step'), 10 xlabel('iteration'),ylabel('value of cost'), 11 legend('value of cost'); 12 13 % 绘右侧图,展示迭代过程中theta的变化曲线 14 theta0_history = theta_history(1,:); 15 theta1_history = theta_history(2,:); 16 subplot(1,2,2); 17 plot(iterX,theta0_history,'-','linewidth',2); 18 hold on; 19 plot(iterX,theta1_history,'-','linewidth',2,'color','r'); 20 title('theta of each step'),xlabel('iteration'),ylabel('value of theta'),legend('theta0','theta1'); 21 % --------------【改动2】绘制代价和theta变化曲线 end -------------- 22 23 % Predict values for population sizes of 35,000 and 70,000 24 predict1 = [1, 3.5] * theta; 25 fprintf('For population = 35,000, we predict a profit of %f ',... 26 predict1*10000); 27 predict2 = [1, 7] * theta; 28 fprintf('For population = 70,000, we predict a profit of %f ',... 29 predict2*10000);

输出如下:

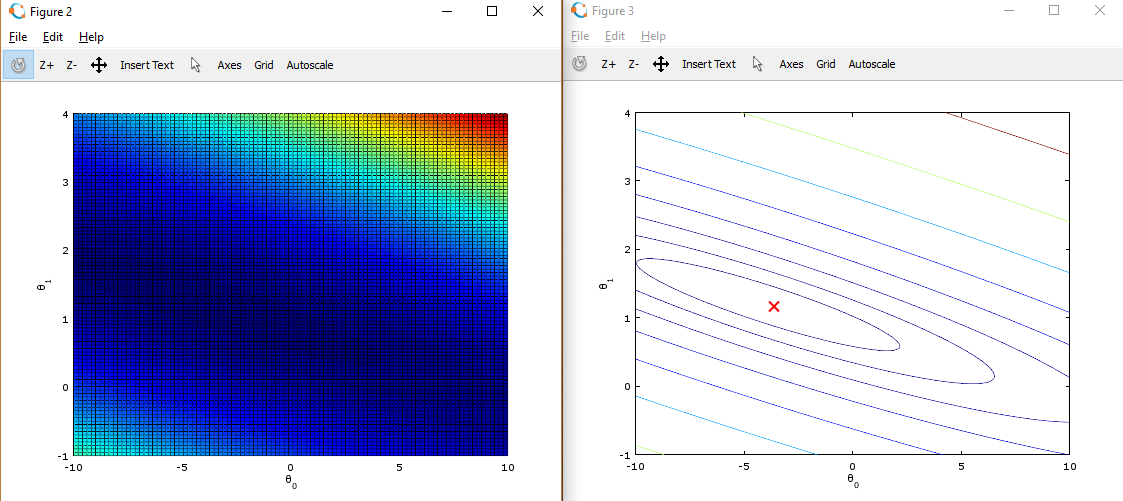

五、绘制代价函数三维曲线 和 等高线图

ex1.m 调用:

1、初始化 theta0 为(-10,10)均分100个点,theta1 为(-1,4)均分100个点,J_vals 为100 * 100的数组

这里使用了Matlab中的均分计算指令 linspace(x1,x2,N) ,用于产生x1、x2之间的N点行线性的矢量。其中x1、x2、N分别为起始值、终止值、元素个数。默认N为100。

2、循环计算每组(theta0,theta1),用 J_vals 保存对应的代价cost。

1 %% ============= Part 4: Visualizing J(theta_0, theta_1) ============= 2 fprintf('Visualizing J(theta_0, theta_1) ... ') 3 4 % Grid over which we will calculate J 5 theta0_vals = linspace(-10, 10, 100); 6 theta1_vals = linspace(-1, 4, 100); 7 8 % initialize J_vals to a matrix of 0's 9 J_vals = zeros(length(theta0_vals), length(theta1_vals)); 10 11 % Fill out J_vals 12 for i = 1:length(theta0_vals) 13 for j = 1:length(theta1_vals) 14 t = [theta0_vals(i); theta1_vals(j)]; 15 J_vals(i,j) = computeCost(X, y, t); 16 end 17 end 18 19 20 % Because of the way meshgrids work in the surf command, we need to 21 % transpose J_vals before calling surf, or else the axes will be flipped 22 J_vals = J_vals'; 23 % Surface plot 24 figure; 25 surf(theta0_vals, theta1_vals, J_vals) 26 xlabel(' heta_0'); ylabel(' heta_1'); 27 28 % Contour plot 29 figure; 30 % Plot J_vals as 15 contours spaced logarithmically between 0.01 and 100 31 contour(theta0_vals, theta1_vals, J_vals, logspace(-2, 3, 20)) 32 xlabel(' heta_0'); ylabel(' heta_1'); 33 hold on; 34 plot(theta(1), theta(2), 'rx', 'MarkerSize', 10, 'LineWidth', 2);

3、将theta0作为X坐标,theta1作为Y坐标,J_vals作为Z坐标,绘制三维图形

4、将theta0作为X坐标,theta1作为Y坐标,绘制J_vals的等高线图

5、在等高线图中,标记上面求出的使代价函数最小的 theta0,theta1点的位置。在等高线中心

这些图像的目的是为了展示 随着Θ0 和 Θ1 的改变,J值的变化。(在2D轮廓图中比3D的更直观)。最小点是Θ0 和 Θ1最适点, 每一步梯度下降都会更靠近这个点。

可以通过旋转看到为什么叫“轮廓图”:

选做 多变量线性回归

一 、特征归一化

需要用特性放缩让数据的范围缩小,使得梯度下降计算的更快:

-

- 计算每个特性的平均值(mean)

- 计算标准差(standard deviations)

- 特性放缩(feature scaling)

* 这里利用的是标准差(standard deviation),也可以使用差值(max - min)。

featureNormalize.m 如下:

1 function [X_norm, mu, sigma] = featureNormalize(X)

7

9 X_norm = X;

10 mu = zeros(1, size(X, 2)); % 1行,列数和X相同

11 sigma = zeros(1, size(X, 2));

12

13 % ====================== YOUR CODE HERE ======================

29 mu = mean(X);

30 sigma = std(X);

32 X_norm = (X_norm - mu) ./ sigma;

35

36 end

二、代价函数和梯度下降

因为在单变量线性回归中,使用的是向量化的计算方法,对于多变量线性回归同样适用。不需要重新写

computeCostMulti.m 和 computCost.m 一样,gradientDescentMulti.m 和gradientDescent.m 一样

ex1_multi.m 里的调用:

1 %% ================ Part 2: Gradient Descent ================ 3 alpha = 1.2; 4 num_iters = 400; 5 6 % Init Theta and Run Gradient Descent 7 theta = zeros(3, 1); 8 [theta,J_history] = gradientDescentMulti(X, y, theta, alpha, num_iters); 9 10 % Plot the convergence graph 11 figure; 12 plot(1:numel(J_history), J_history, '-b', 'LineWidth', 2); 13 xlabel('Number of iterations'); 14 ylabel('Cost J'); 15 16 % Estimate the price of a 1650 sq-ft, 3 br house 17 % 这里要注意,需要把输入的值进行 normalize,然后才能代入预测方程中 18 predict_x = [1650,3]; 19 predict_x = (predict_x - mu) ./ sigma; 20 price = [1, predict_x] * theta;

三、正规方程

公式:

![]()

normalEqn.m 实现:

1 function [theta] = normalEqn(X, y) 6 theta = zeros(size(X, 2), 1); 12 theta = pinv(X' * X) * X' * y 15 end

ex1_multi 里的调用:

1 %% ================ Part 3: Normal Equations ================ 6 % predict the price of a 1650 sq-ft, 3 br house.10 data = csvread('ex1data2.txt'); % 重新加载数据 11 X = data(:, 1:2); 12 y = data(:, 3); 13 m = length(y); 14 15 % Add intercept term to X 16 X = [ones(m, 1) X]; 17 18 % Calculate the parameters from the normal equation 19 theta = normalEqn(X, y); % 使用正规方程进行计算25

28 % ====================== YOUR CODE HERE ======================

29 price = [1, 1650, 3] * theta; % 预测结果 30 31 % ============================================================

四、测试

运行结果:

1 Loading data ... 2 First 10 examples from the dataset: 3 x = [2104 3], y = 399900 4 x = [1600 3], y = 329900 5 x = [2400 3], y = 369000 6 x = [1416 2], y = 232000 7 x = [3000 4], y = 539900 8 x = [1985 4], y = 299900 9 x = [1534 3], y = 314900 10 x = [1427 3], y = 198999 11 x = [1380 3], y = 212000 12 x = [1494 3], y = 242500 13 Program paused. Press enter to continue. 14 Normalizing Features ... 15 1.00000000 0.13000987 -0.22367519 16 1.00000000 -0.50418984 -0.22367519 17 1.00000000 0.50247636 -0.22367519 18 1.00000000 -0.73572306 -1.53776691 19 1.00000000 1.25747602 1.09041654 20 1.00000000 -0.01973173 1.09041654 21 1.00000000 -0.58723980 -0.22367519 22 1.00000000 -0.72188140 -0.22367519 23 1.00000000 -0.78102304 -0.22367519 24 1.00000000 -0.63757311 -0.22367519 25 1.00000000 -0.07635670 1.09041654 26 1.00000000 -0.00085674 -0.22367519 27 1.00000000 -0.13927334 -0.22367519 28 1.00000000 3.11729182 2.40450826 29 1.00000000 -0.92195631 -0.22367519 30 1.00000000 0.37664309 1.09041654 62 Running gradient descent ... 63 Theta computed from gradient descent: 64 334302.063993 65 100087.116006 66 3673.548451

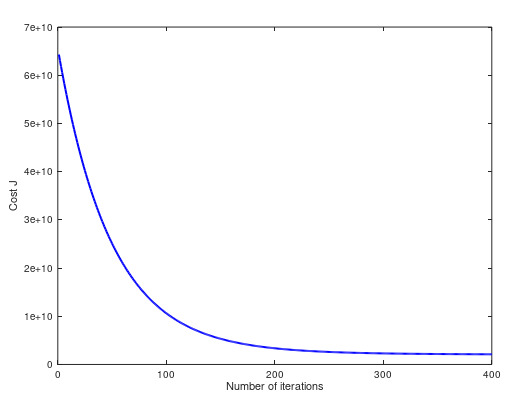

(1)当 α = 0.05,预测一个1650 sq-ft, 3 br house 的房屋的售价。梯度下降和正规方程的预测值不同:

68 Predicted price of a 1650 sq-ft, 3 br house (using gradient descent):

69 $289314.620338

81

82 Predicted price of a 1650 sq-ft, 3 br house (using normal equations):

83 $293081.464335

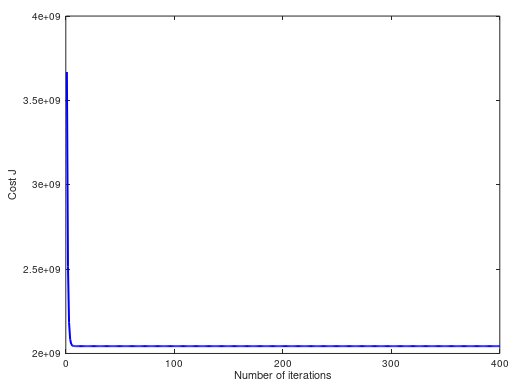

(2)当 α = 0.15,cost 曲线如下。两个方法预测值都是 $293081.464335:

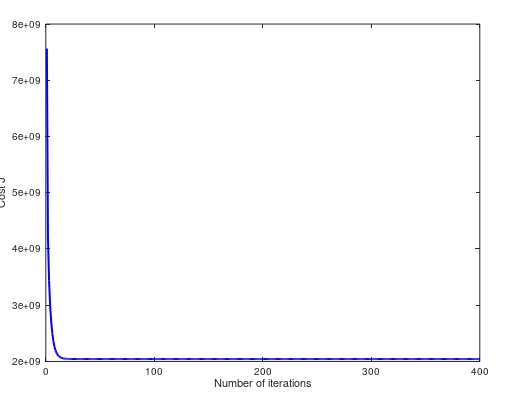

(3)当 α = 1,cost 曲线如下。两个方法预测值都是 $293081.464335:

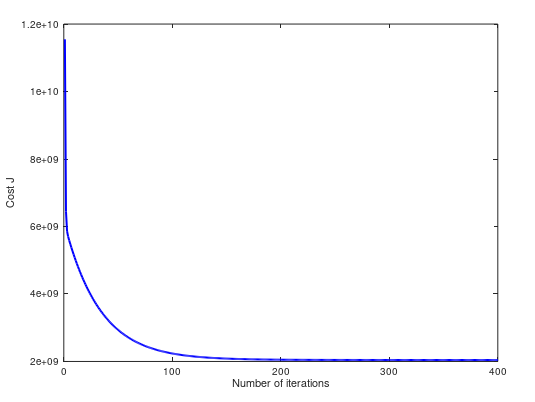

(4)当 α = 1.2,cost 曲线如下。两个方法预测值都是 $293081.464335:

(5)当 α = 1.3,cost 曲线如下。两个方法预测值不同 $293157.248289 ,$293081.464335:

完整代码:https://github.com/madoubao/coursera_machine_learning/tree/master/homework/machine-learning-ex1/ex1