泊松分布描述的是给定的某段时间内,事件发生的概率

1.Poisson Process

1.1 Counting process

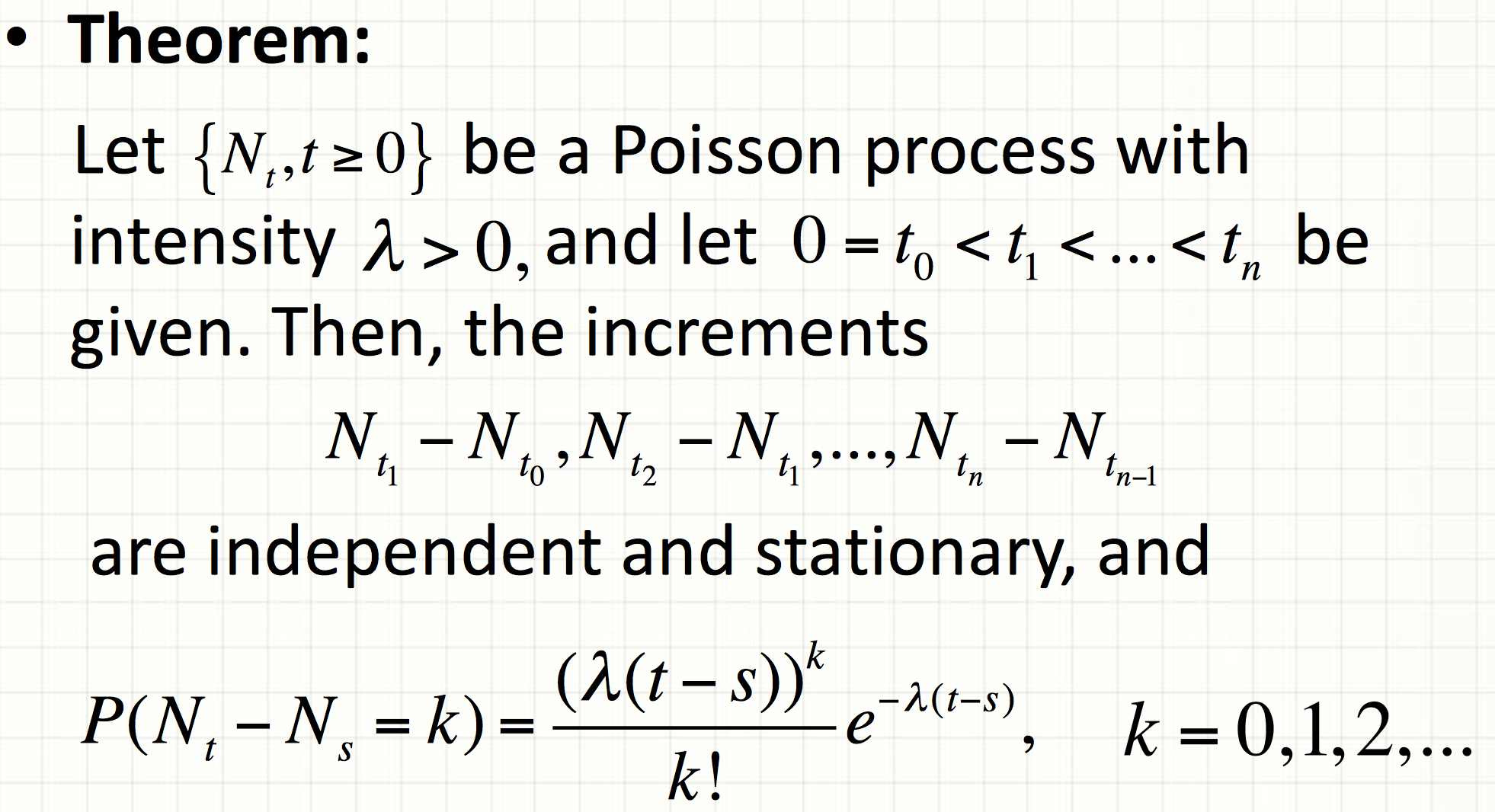

independent increment

注:增量是独立并且稳定的,同样服从泊松分布!!!!这个实际上是无记忆性!

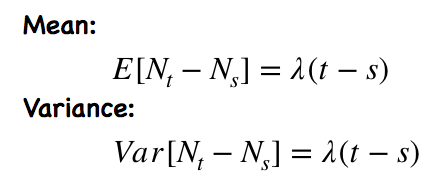

Mean, Variance

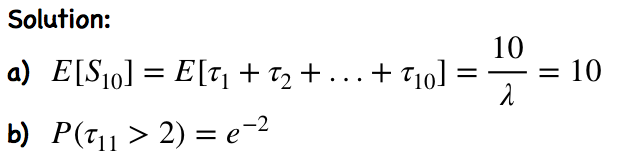

下面通过例子理解:

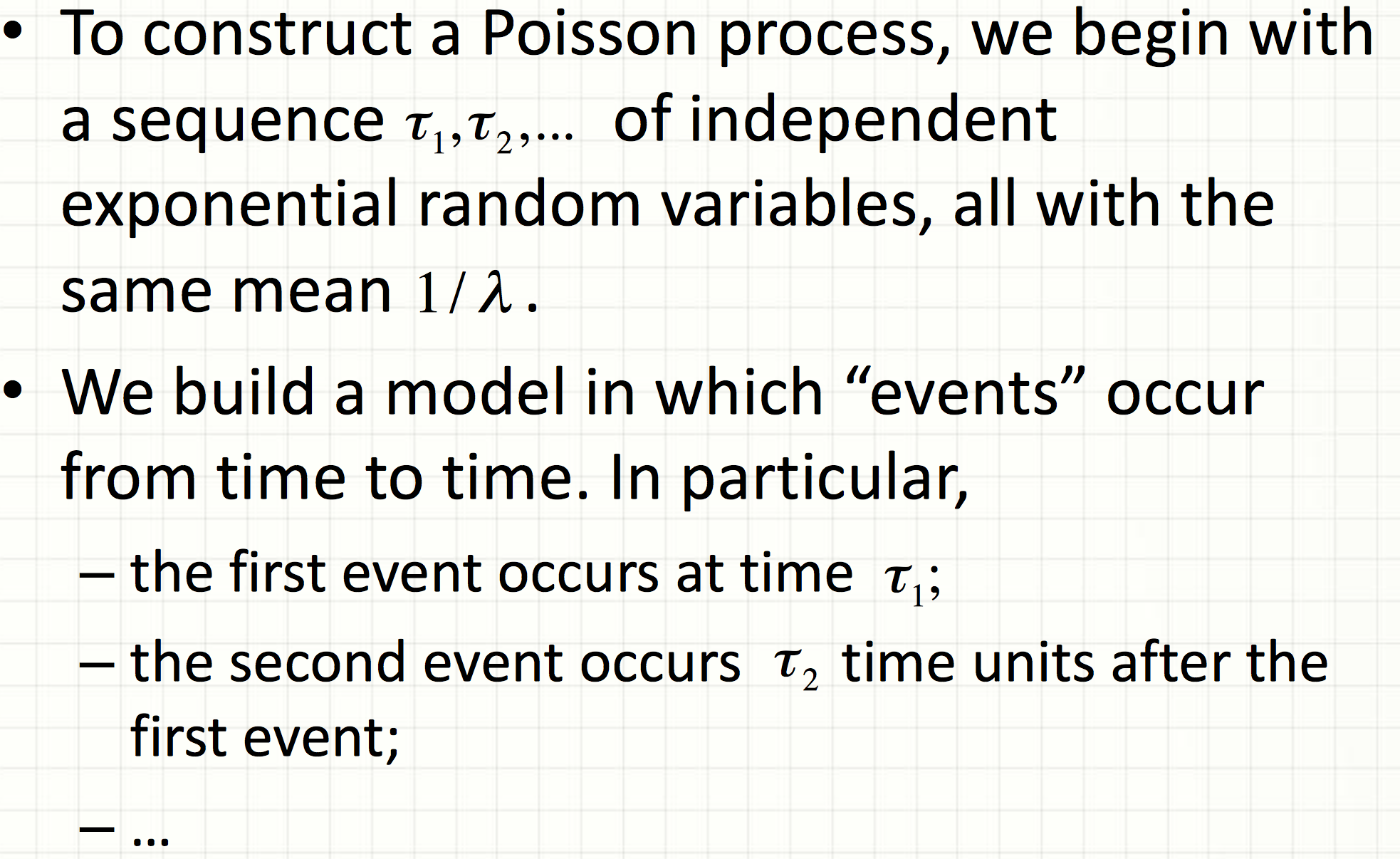

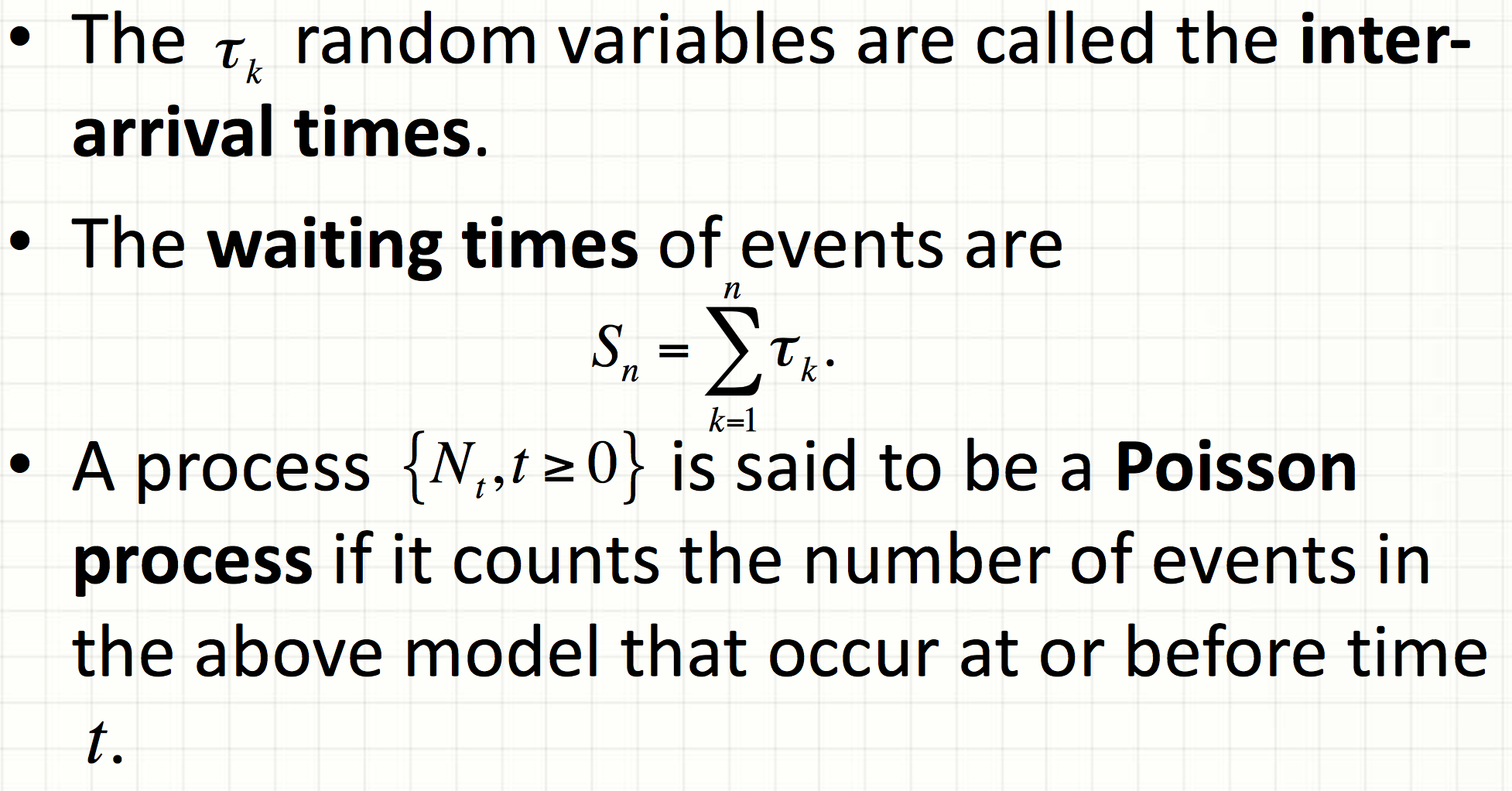

如何构建泊松过程:

泊松过程描述的是给定的时间t之前发生的事件总数!!

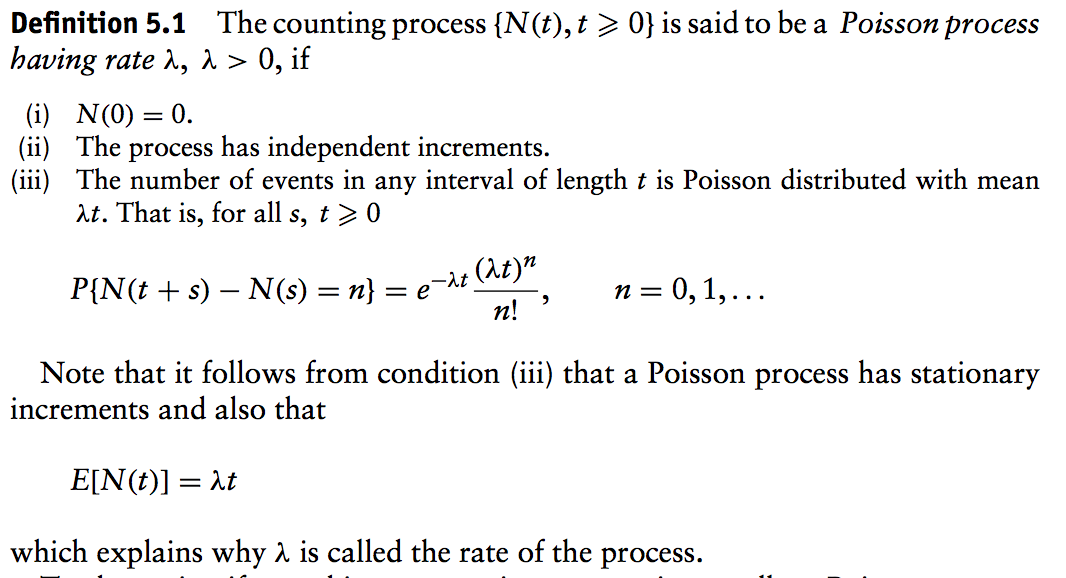

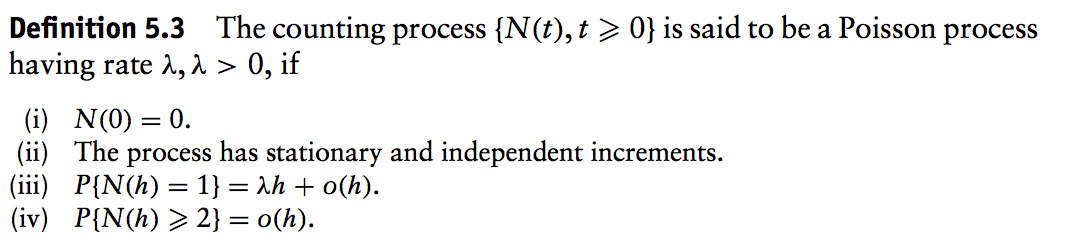

1.2 Definition

关于泊松分布的定义,有以下两种

1.3 Properties

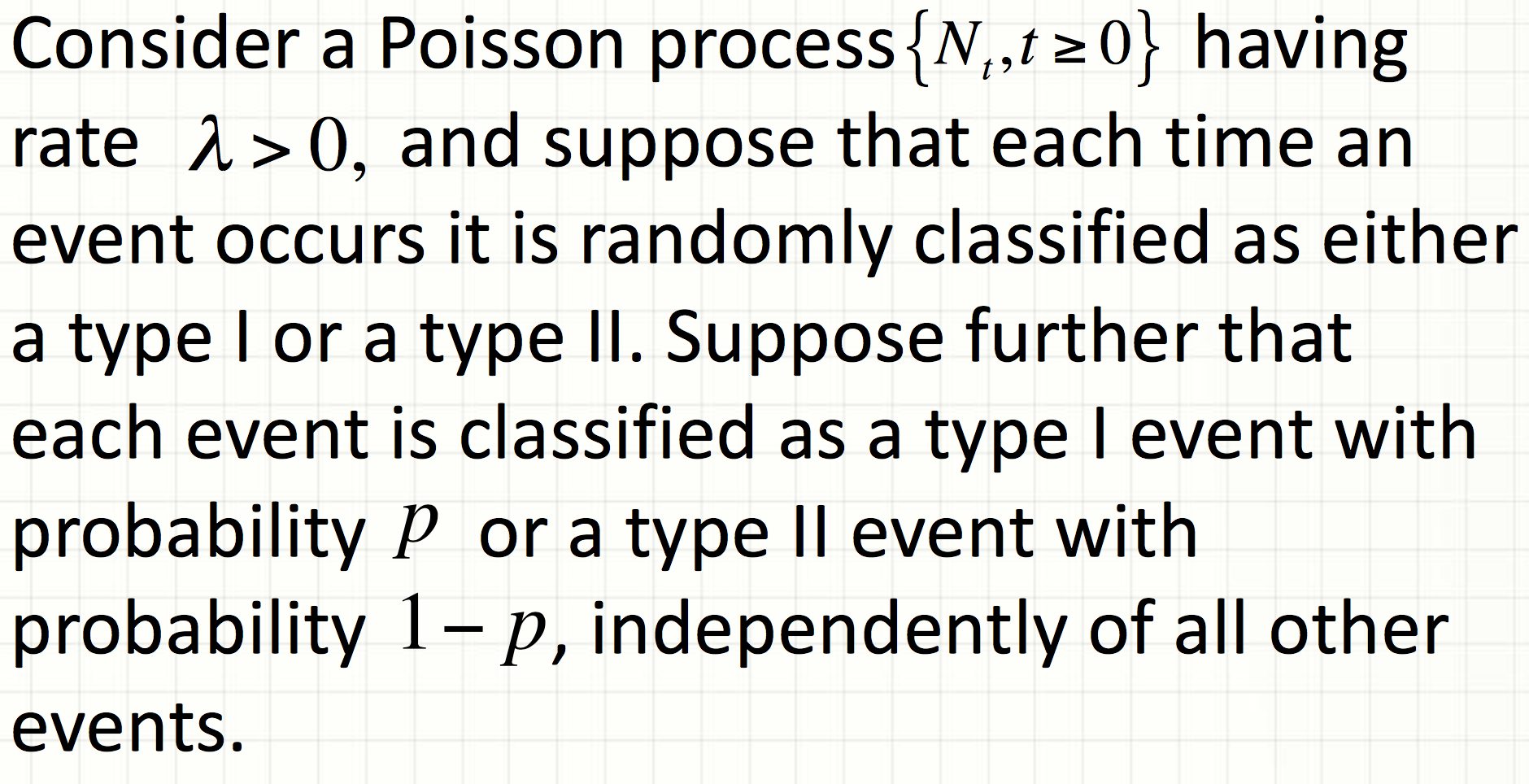

1.3.1 Decomposition

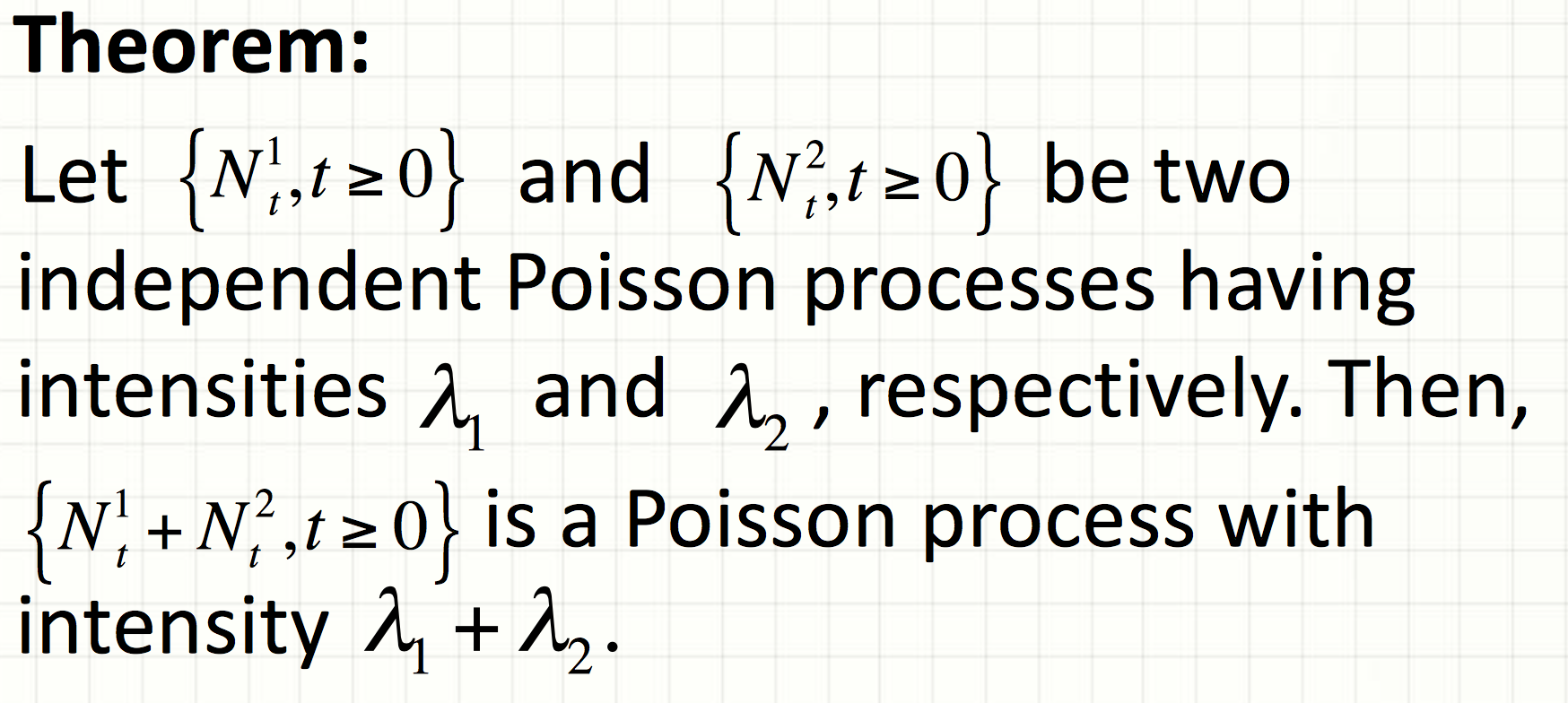

1.3.2 Superposition

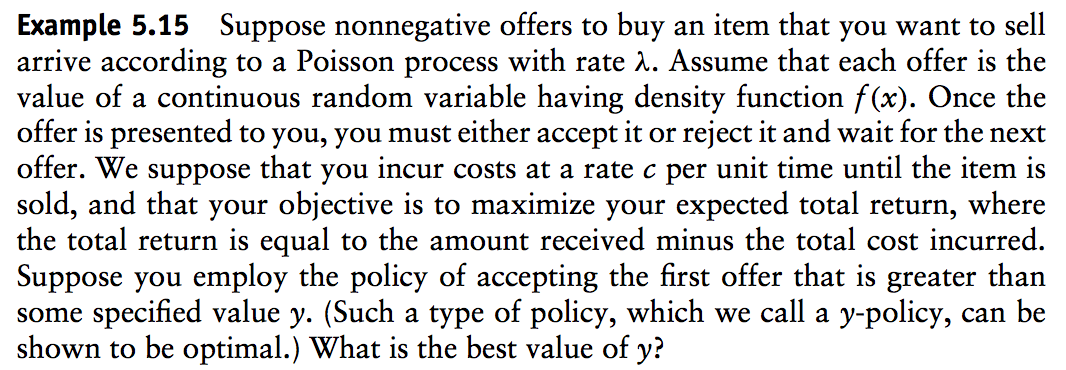

举例应用:

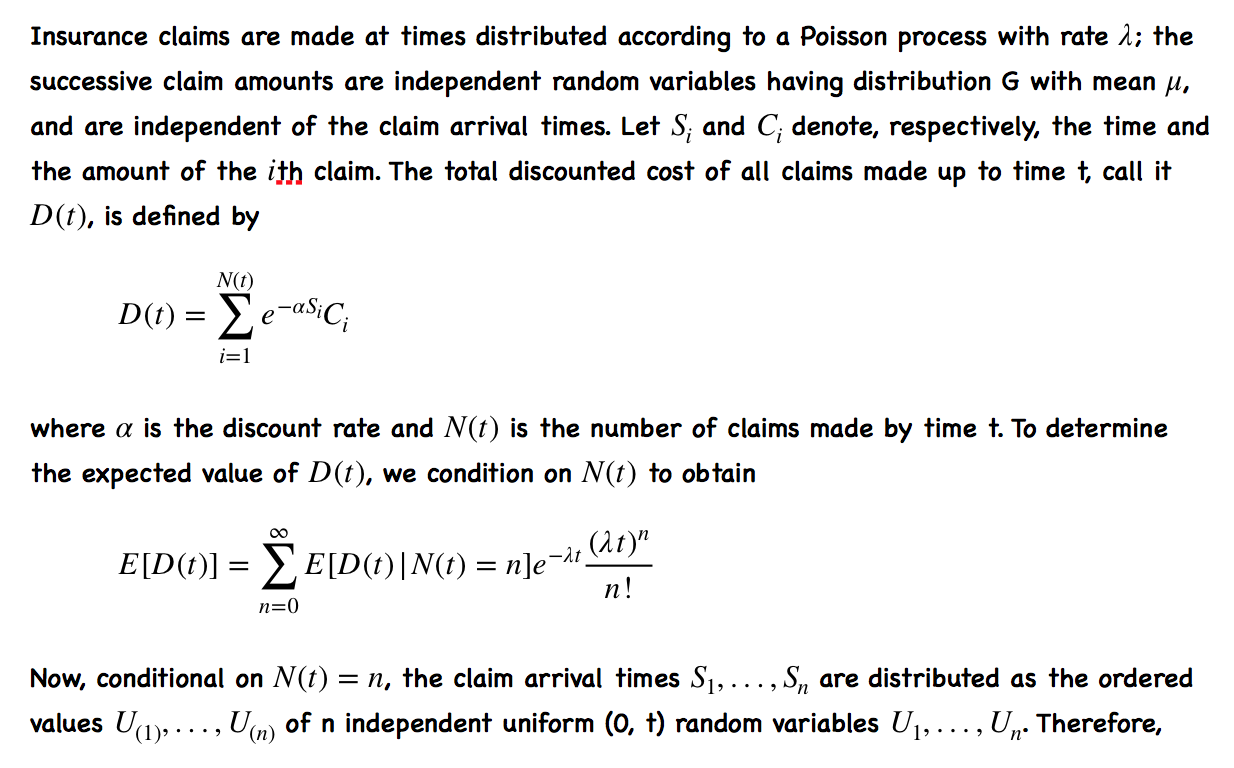

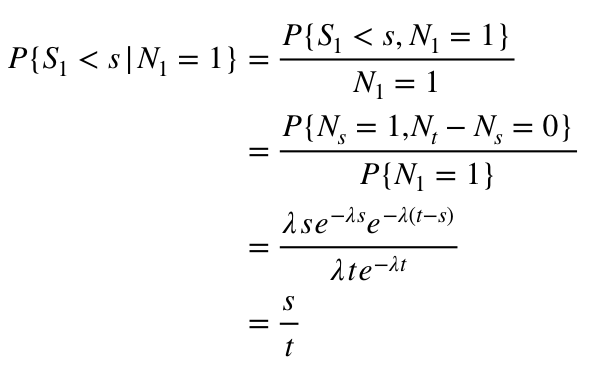

1.4 Conditioanal distribution of arrival times

1.4.1

-

In other words, the time of the event should be uniformly distributed over [0, t].

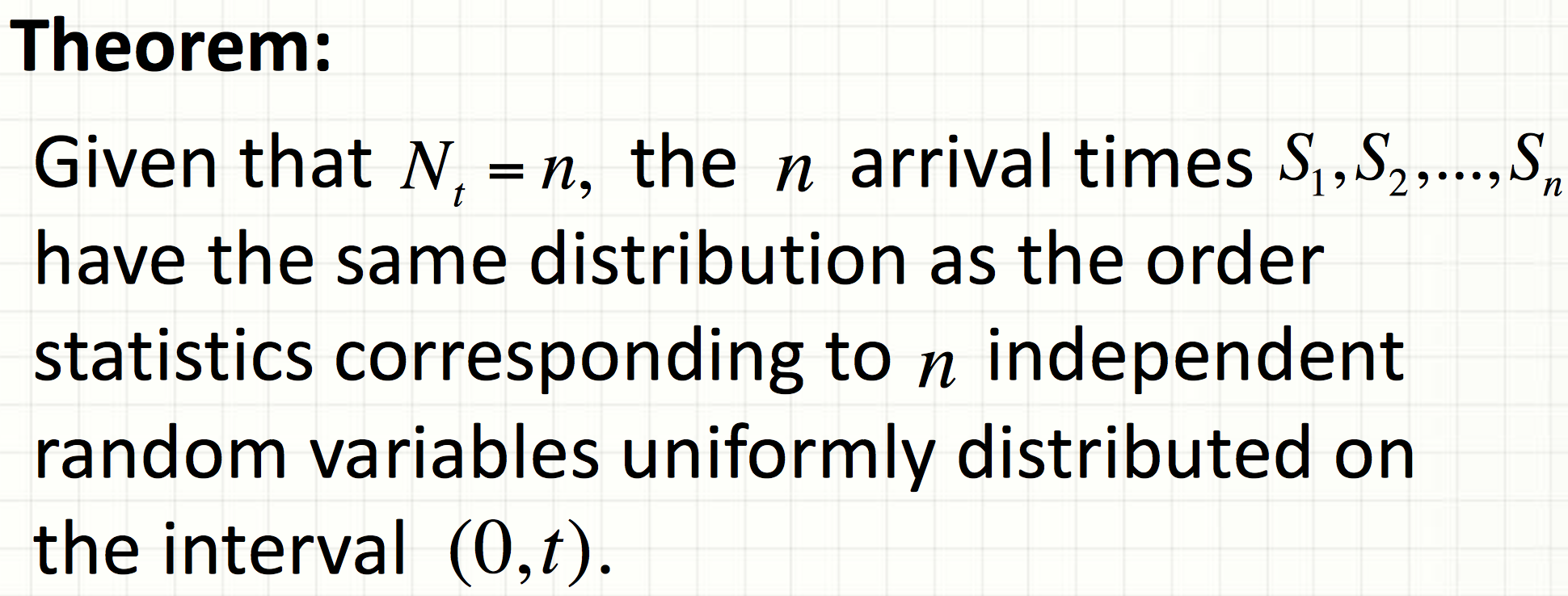

1.4.2 Order statistics

-

Let Y1,Y2,...,Yn be n random variables. We say that Y(1),Y(2),...,Y(n) are the corresponding order statistics if Y(k) is the k th smallest

value among Y1,Y2,...,Yn.

-

For instance,

(Y1,Y2,Y3)=(4,5,1)

The corresponding order statistics are(Y(1),Y(2),Y(3))=(1,4,5).

下面是例子: